Understanding Offshore Company Formations: A Comprehensive Guide to the Process and Benefits

Offshore firm formations present a critical method for entrepreneurs looking for to optimize their company operations. These entities often supply benefits such as tax advantages, increased personal privacy, and durable asset defense. Recognizing the complexities of picking a territory, the formation process, and compliance demands is essential. As the landscape of worldwide service evolves, the implications of establishing an offshore business warrant mindful factor to consider. What steps should one require to navigate this complex surface?

What Is an Offshore Business?

An overseas firm is a company entity included outside the territory of its owners' residence, typically in a nation with desirable regulatory and tax atmospheres. These business can offer numerous objectives, consisting of property defense, international trading, and wide range management. They are generally established in jurisdictions understood as tax sanctuaries, where business tax rates are low or nonexistent, and personal privacy regulations are rigorous.

Offshore firms may be possessed by individuals or various other corporate entities and can operate in various sectors, including finance, consulting, and shopping. While they offer certain benefits, the lawful and regulative structures regulating offshore firms differ significantly by jurisdiction. Company owner should navigate these intricacies to ensure compliance with both international and regional laws. Understanding the structure and function of offshore companies is necessary for people considering this choice for company procedures or possession management.

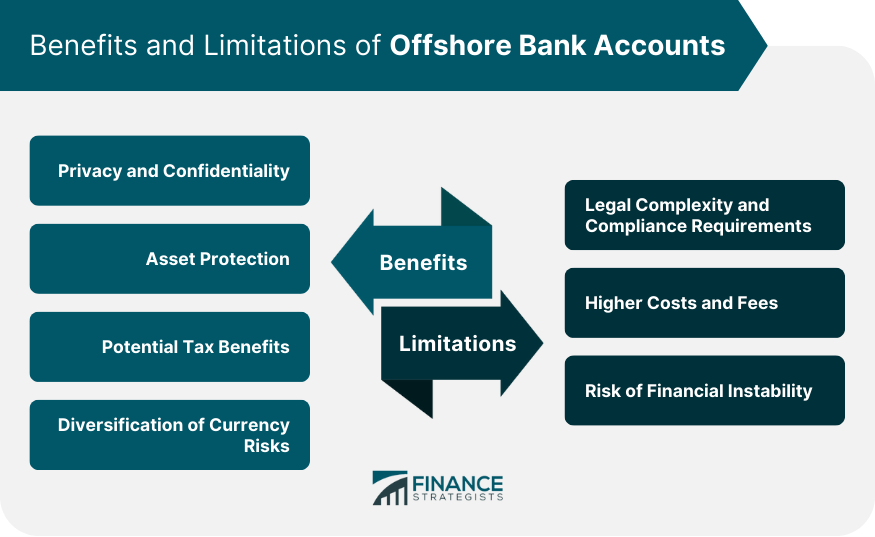

Advantages of Forming an Offshore Firm

While the decision to create an overseas business might come from various critical considerations, the possible benefits are compelling for several local business owner. One considerable benefit is tax optimization; many offshore territories provide desirable tax prices or perhaps tax exceptions, allowing business to preserve more revenues. In addition, offshore firms typically give improved personal privacy defense, shielding the identifications of investors and directors from public examination.

Business owners might find operational adaptability, as offshore jurisdictions regularly have fewer regulative difficulties, enabling streamlined administration and administration. Collectively, these benefits make offshore firm formations an appealing alternative for lots of looking for to expand their service perspectives.

Choosing the Right Jurisdiction

Choosing the ideal territory for an offshore company is a crucial action in maximizing the advantages detailed previously. Numerous aspects influence this decision, including tax obligation laws, company laws, and the overall company atmosphere. Jurisdictions such as the British Virgin Islands, Cayman Islands, and Singapore are usually favored for their favorable tax routines and durable lawful frameworks.

It is vital to take into account the particular requirements of the organization, such as privacy requirements and regulative conformity. Additionally, the ease of doing service, consisting of the performance of firm registration and financial centers, plays a significant role.

Prospective owners ought to also assess the political stability and credibility of the selected jurisdiction, as these components can influence lasting success. Eventually, detailed research study and expert assessment are recommended to guarantee placement with the firm's objectives and to take advantage of the full possibility of overseas advantages.

The Offshore Business Development Refine

The offshore company formation procedure entails a collection of crucial actions that need mindful planning and execution. Individuals or services have to pick an ideal territory that straightens with their objectives, considering factors such as tax benefits, privacy, and regulatory environment. Following this, the next action requires picking the appropriate business structure, such as an International Business Business (IBC) or Minimal Responsibility Firm (LLC)

As soon as the framework is established, essential records, consisting of an organization plan, identification, and proof of address, must be prepared. Involving a trusted local agent or service company can improve this phase, ensuring conformity with regional policies. After submitting the called for documents to the appropriate authorities, the formation procedure commonly culminates in the issuance of a certificate of incorporation. This document develops the company as a legal entity, permitting it to carry out company internationally.

Lawful Demands and Compliance

Understanding the lawful requirements and compliance obligations is necessary for any individual seeking to develop an overseas business. Each jurisdiction has certain policies that should be complied with, which can include firm registration, getting required licenses, and keeping regional addresses. Offshore Company Formations. It is important to assign a registered representative that can assist in interaction with regional authorities and warranty compliance with continuous coverage demands

In addition, numerous territories need the entry of annual monetary declarations, along with tax obligation filings, even if the firm does not generate earnings. Supervisors and investors need to be identified, with due diligence treatments often mandated to verify their identities. Failing to meet these legal obligations can lead to fines or the dissolution of the firm. Therefore, possible overseas company proprietors should speak with attorneys experienced in international company regulation to browse these intricacies efficiently and ensure complete conformity with all laws.

Tax Ramifications of Offshore Business

The tax obligation effects of offshore business existing substantial advantages that draw in lots of entrepreneurs. Recognizing the connected conformity demands is essential for steering the intricacies of international tax obligation legislations. This area will certainly explore both the possible advantages and the essential obligations connected to offshore business frameworks.

Tax Benefits Introduction

Although overseas business are often viewed with hesitation, they can provide significant tax benefits for people and organizations looking for to optimize their economic strategies. Among the main benefits is the potential for lower company tax obligation rates, which can bring about significant financial savings. Numerous overseas territories offer favorable tax obligation routines, including absolutely no or very little tax obligation on revenues, capital gains, and inheritance. In addition, overseas business can help with international organization procedures by lowering tax liabilities connected with cross-border deals. This structure might additionally make it possible for tax obligation deferral opportunities, permitting earnings to grow without instant taxes. Eventually, these advantages add to improved financial efficiency and possession defense, making offshore business an attractive choice for savvy capitalists and entrepreneurs.

Compliance Demands Discussed

Offshore firms may offer tax benefits, but they additionally include a set of compliance requirements that need to be very carefully navigated. These entities undergo certain reporting commitments, which vary substantially depending on the jurisdiction. Commonly, offshore business need to keep accurate monetary documents and submit yearly financial statements to abide by local laws. Furthermore, many jurisdictions call for the disclosure of valuable you can look here ownership to fight cash laundering and tax evasion. Failing to follow these conformity steps can lead to serious penalties, including fines and potential loss of company licenses. Comprehending the regional tax laws and international agreements is necessary, as they can affect tax responsibilities and total functional validity. Involving with lawful and financial experts is recommended to assure complete compliance.

Maintaining and Handling Your Offshore Business

Maintaining and taking care of an overseas business involves sticking to different ongoing conformity needs necessary for legal operation. This consists of thorough financial document maintaining and an understanding of tax obligation responsibilities essential to the business's territory. Efficient management not just ensures regulatory conformity but additionally supports the firm's monetary health and long life.

Continuous Conformity Demands

Guaranteeing continuous conformity is crucial for any entity operating in the overseas sector, as failing to meet regulative needs can cause significant charges or perhaps dissolution of the business. Offshore firms should follow local legislations, which might include annual filing of financial declarations, payment of needed charges, and preserving a licensed office address. Additionally, business are typically called for to designate a regional representative or representative to promote communication with authorities. Regular updates on modifications in regulation or tax demands are important for compliance. Adherence to anti-money laundering (AML) and know-your-customer (KYC) guidelines is imperative. By preserving arranged documents and remaining educated, offshore companies can guarantee they stay compliant and minimize risks related to non-compliance.

Financial Record Maintaining

Reliable financial record keeping is vital for the effective monitoring of any kind of overseas firm. Maintaining accurate and detailed economic documents help in tracking the business's efficiency, guaranteeing conformity with neighborhood laws, and facilitating informed decision-making. Companies need to apply organized procedures for documenting earnings, expenses, and purchases to develop transparency and liability. Utilizing accounting software can simplify this procedure, enabling for real-time financial analysis and coverage. Routinely reviewing economic declarations assists identify fads, analyze productivity, and handle cash circulation efficiently. In addition, it is crucial to firmly save these records to safeguard delicate details and assurance very easy access during audits or financial testimonials. By focusing on meticulous financial record maintaining, overseas companies can enhance functional effectiveness and assistance long-lasting success.

Tax Obligation Commitments Summary

Recognizing tax commitments is essential for the appropriate monitoring of an offshore business, as it straight impacts economic performance and compliance. Offshore firms may undergo different tax obligation laws relying on their jurisdiction, including business tax obligations, value-added taxes, and withholding taxes. It is vital for local business owner to stay informed regarding their tax obligation responsibilities, as failure to conform can cause fines and legal problems. Furthermore, several offshore jurisdictions use tax obligation incentives, which can considerably profit businesses if browsed correctly. Engaging an experienced tax obligation expert or accounting professional specializing in international tax law can assist assure that firms fulfill their obligations while enhancing their tax strategies. Ultimately, attentive tax administration contributes to the general success and sustainability of an overseas entity.

Often Asked Concerns

Can I Open a Checking Account for My Offshore Company From Another Location?

The capacity to open up a savings account for an overseas business remotely depends on the financial institution's plans and the territory's policies. Many banks supply remote solutions, however certain demands might differ significantly between institutions.

What Are the Costs Associated With Creating an Offshore Firm?

The expenses involved in creating an overseas company normally include registration costs, lawful and consulting expenses, and recurring upkeep fees. These expenses vary substantially based upon territory, complexity of the business framework, and certain solutions called for.

Are There Restrictions on That Can Be a Shareholder?

Constraints on shareholders differ by jurisdiction. Some nations may impose restrictions based on residency, service, or citizenship type - Offshore Company Formations. It's necessary for potential financiers to research certain regulations applicable to their selected offshore area

The length of time Does the Offshore Business Development Process Generally Take?

The offshore firm formation procedure usually takes between a couple of days to several weeks. Factors affecting the timeline include territory requirements, record preparation, and responsiveness of More Bonuses relevant authorities associated with the enrollment procedure.

What Takes place if I Fail to Abide By Local Legislations?

Failing to adhere to local laws can lead to serious penalties, consisting of penalties, lawful activity, or loss of organization licenses - Offshore check Company Formations. It may likewise harm the firm's credibility and prevent future organization opportunities in the jurisdiction

An overseas company is a company entity included outside the jurisdiction of its proprietors' residence, commonly in a country with positive governing and tax obligation atmospheres. One considerable advantage is tax optimization; many overseas territories use positive tax rates or also tax obligation exceptions, enabling business to maintain even more earnings. Overseas business are often checked out with skepticism, they can use significant tax obligation advantages for people and services seeking to optimize their economic techniques. Additionally, overseas business can facilitate worldwide company operations by decreasing tax obligation liabilities associated with cross-border transactions. Offshore firms may be subject to various tax obligation laws depending on their territory, consisting of business taxes, value-added tax obligations, and withholding taxes.

Comments on “Offshore Company Formations Explained: A Thorough Resource for Starters”